Explainable AI with SHAP

Understanding SHAP in Credit Risk

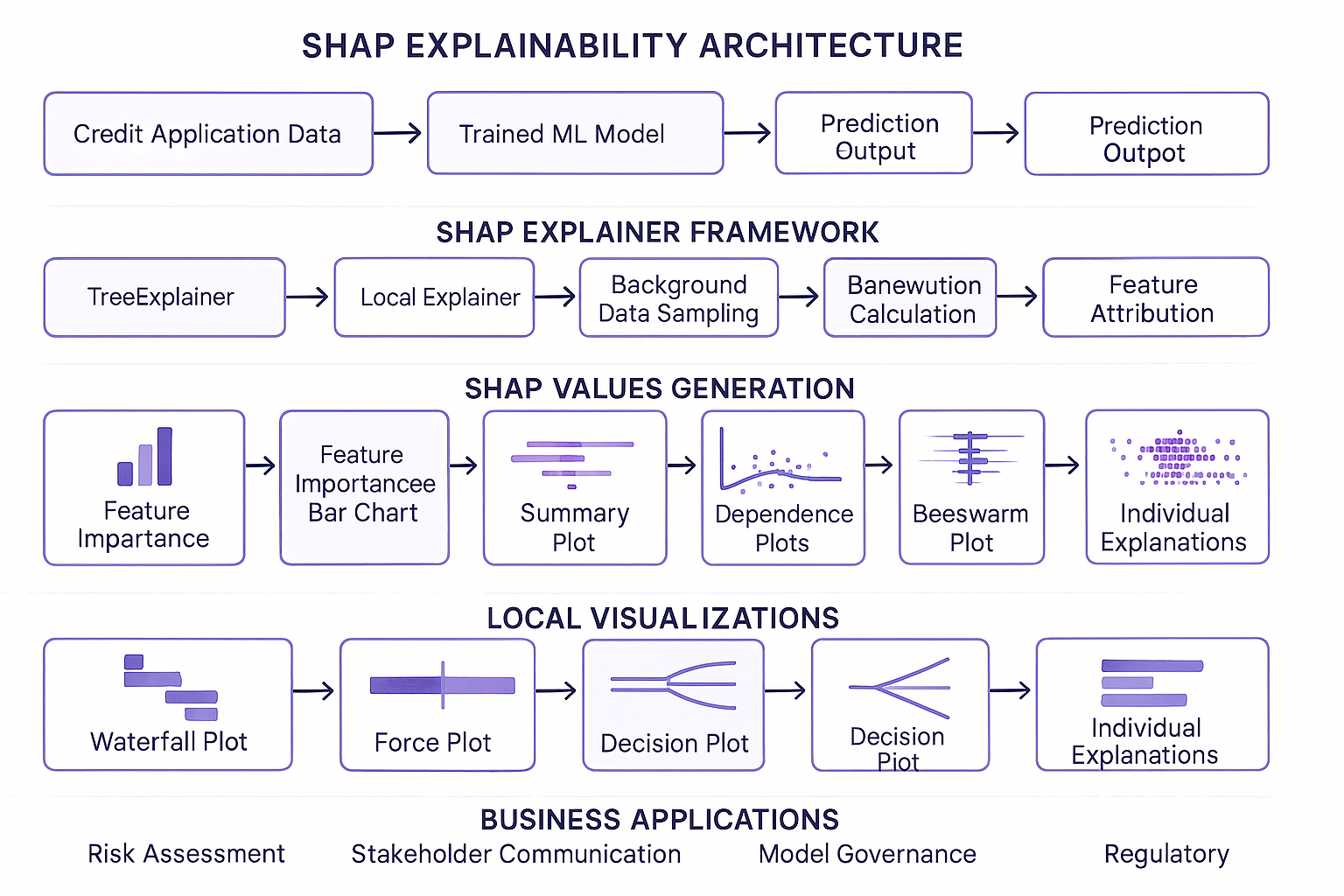

SHAP explanations help us understand which features to focus on to understand why credit default happened. For example, if a customer has high credit utilization (90% of credit limit) and recent payment delays, SHAP will show exactly how much each factor contributes to the high default risk prediction.

Business Example

Why Explainability Matters

- Regulatory compliance (Fair Credit Reporting Act)

- Customer trust and transparency

- Business insight for strategy improvement

- Model debugging and bias detection

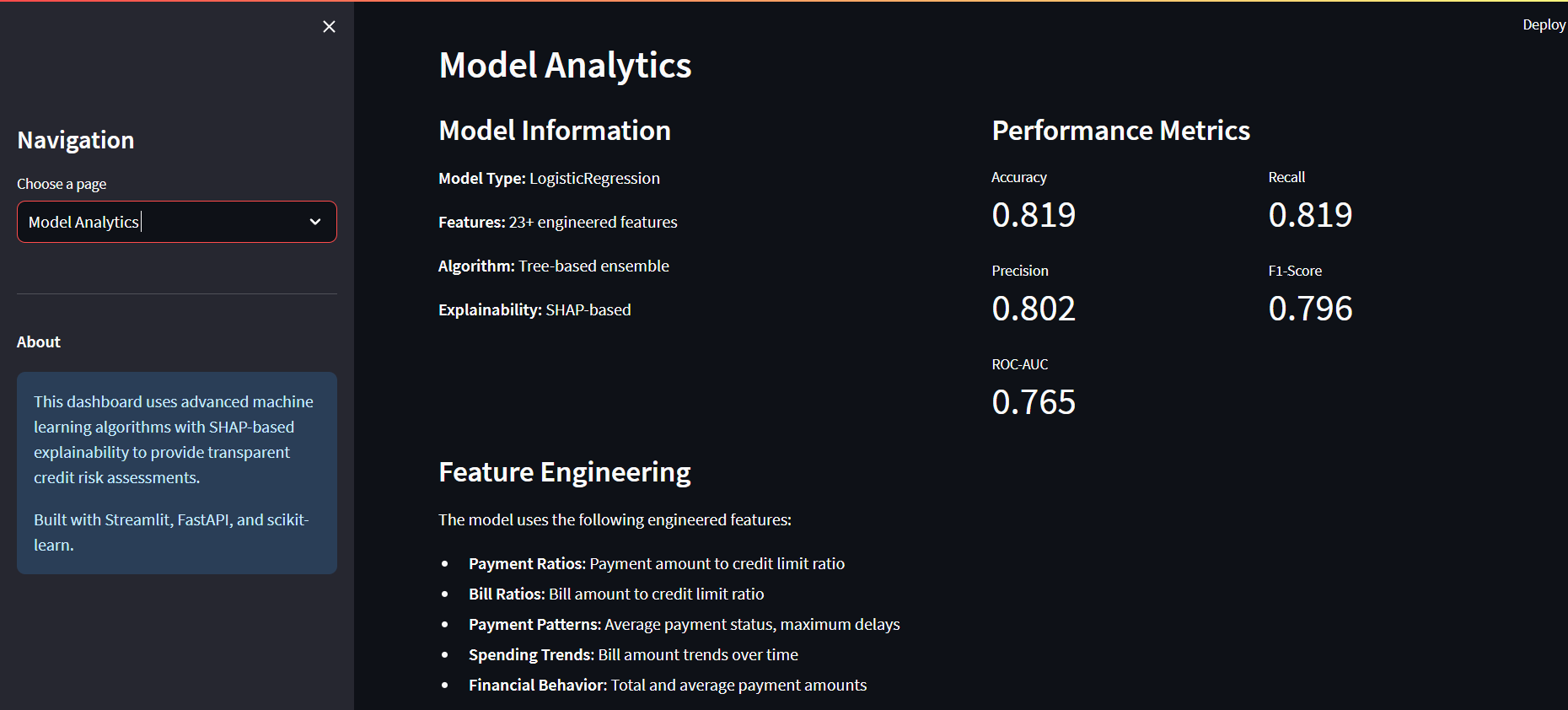

SHAP Implementation

Comprehensive SHAP integration providing both global feature importance and local explanations for individual predictions.

# SHAP Explainer Implementation

import shap

import numpy as np

import pandas as pd

class CreditDefaultSHAPExplainer:

def __init__(self, model, X_train, feature_names):

self.model = model

self.feature_names = feature_names

self.explainer = shap.TreeExplainer(model)

self.shap_values = self.explainer.shap_values(X_train)

def get_global_importance(self):

"""Global feature importance across all predictions"""

importance = np.abs(self.shap_values).mean(0)

return pd.DataFrame({

'feature': self.feature_names,

'importance': importance

}).sort_values('importance', ascending=False)

def explain_prediction(self, instance):

"""Local explanation for single prediction"""

shap_values = self.explainer.shap_values(instance.reshape(1, -1))

return shap_values[0]

Global Explanations

Understand overall model behavior and feature importance across the entire dataset. Shows which features are most influential for default prediction in general.

- Feature importance ranking

- SHAP summary plots

- Dependence plots

Local Explanations

Explain individual predictions by showing exactly how each feature contributed to the specific customer's risk assessment.

- Individual prediction breakdown

- SHAP waterfall plots

- Force plots for decision factors

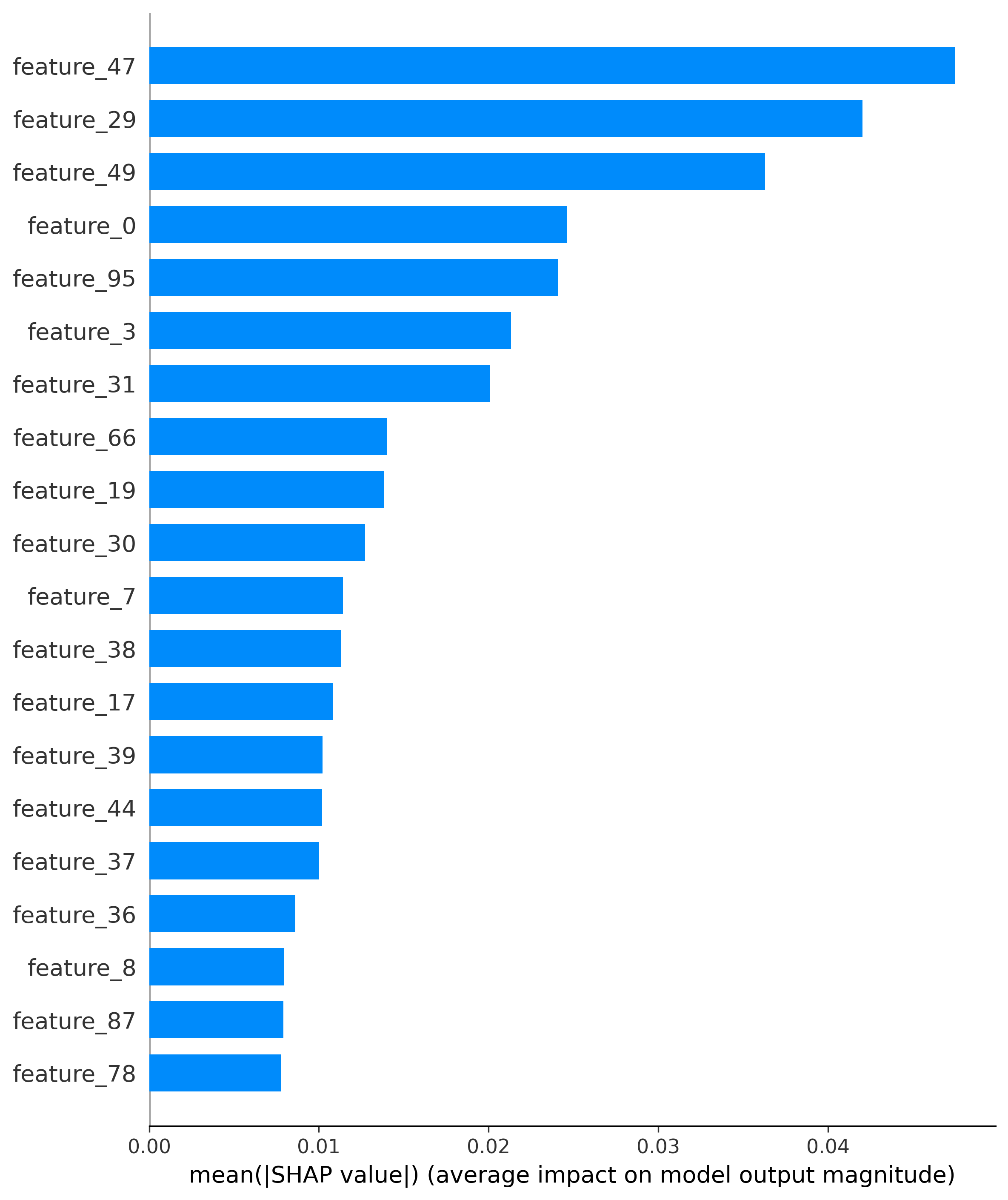

Feature Importance Visualization

Add Feature Importance Plot Image URL Here

This chart shows the most important features for credit default prediction, with payment history and credit utilization being top predictors.

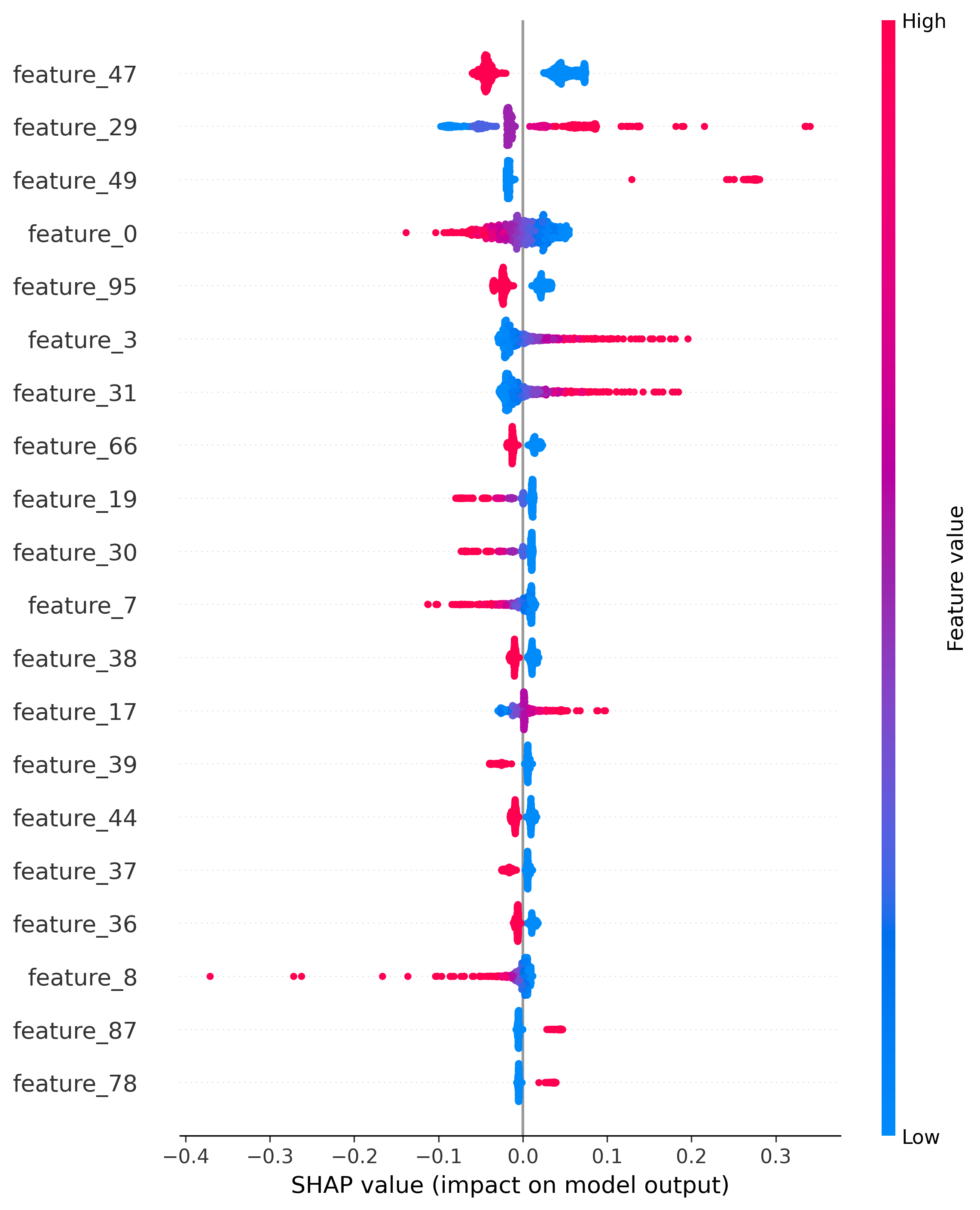

SHAP Summary Plot

Add SHAP Summary Plot Image URL Here

Summary plot shows the distribution of SHAP values for each feature, indicating both positive and negative contributions to default risk.